ŔÖÓăĚĺÓýąŮÍř Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

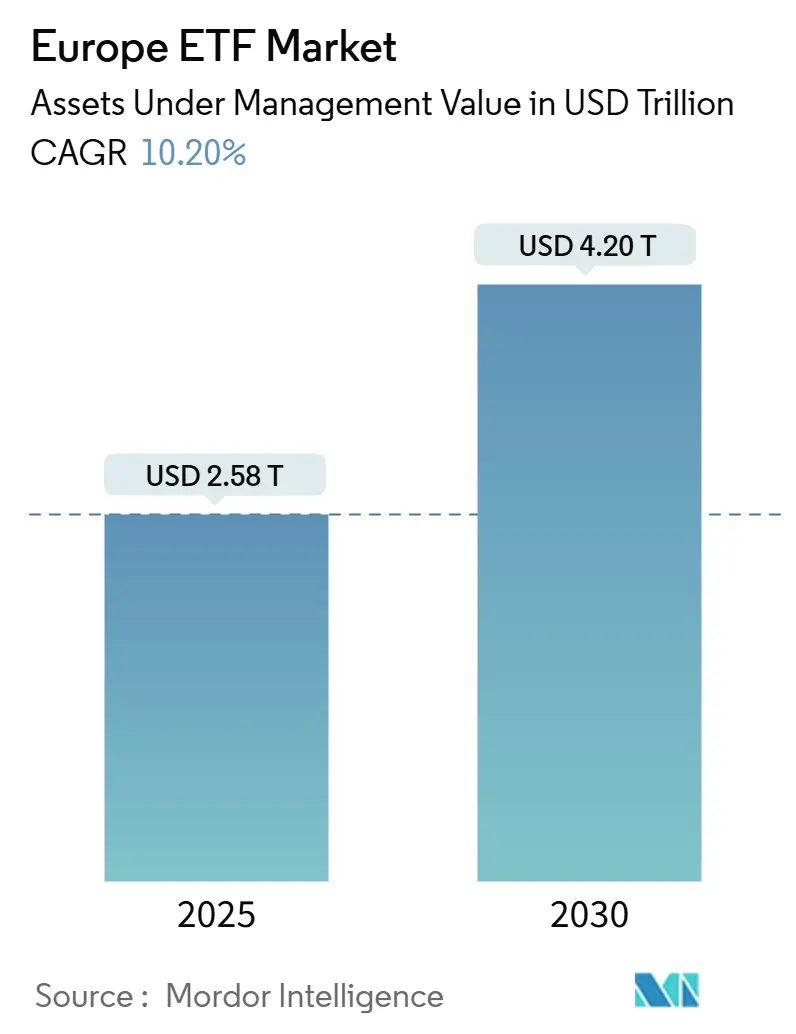

| ŔÖÓăĚĺÓýąŮÍř Size (2025) | USD 2.58 Trillion |

| ŔÖÓăĚĺÓýąŮÍř Size (2030) | USD 4.20 Trillion |

| Growth Rate (2025 - 2030) | 10.20% CAGR |

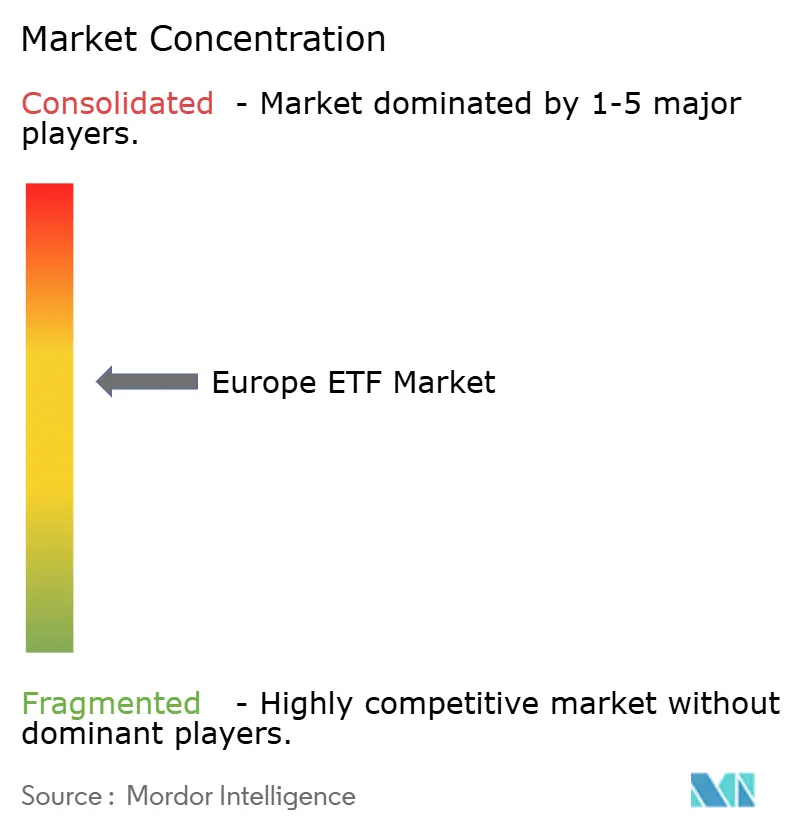

| ŔÖÓăĚĺÓýąŮÍř Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe ETF ŔÖÓăĚĺÓýąŮÍř Analysis by Mordor Intelligence

The Europe ETF ŔÖÓăĚĺÓýąŮÍř size stands at USD 2.58 trillion in 2025 and is forecasted to reach USD 4.20 trillion by 2030, reflecting a 10.20% CAGR. Growth is propelled by MiFID II fee-transparency pressure, regulatory incentives for low-cost vehicles, and rapid digitization of distribution. Product innovation in active, thematic, and ESG strategies is broadening the appeal of exchange-traded funds, while the planned transition to T+1 settlement is expected to improve post-trade efficiency once operational hurdles are resolved. Intensifying competition among global and regional asset managers continues to compress fees, yet it also accelerates product breadth, especially in fixed-income and alternatives. Taken together, these factors confirm the structural realignment of European portfolios toward exchange-traded formats and suggest further penetration into both institutional mandates and retail savings plans.

Key Report Takeaways

- By asset class, equity led with 67.8% of the Europe ETF ŔÖÓăĚĺÓýąŮÍř share in 2024; alternatives are projected to expand at a 13.72% CAGR through 2030.

- By investment strategy, passive products retained 90.7% of the Europe ETF ŔÖÓăĚĺÓýąŮÍř share in 2024, while active strategies are expected to grow at a 15.21% CAGR to 2030.

- By investor type, institutional investors held 62.5% of the Europe ETF ŔÖÓăĚĺÓýąŮÍř size in 2024; the retail segment is projected to advance at an 11.43% CAGR between 2025-2030.

- By distribution channel, institutional platforms accounted for 37.9% of flows in 2024, whereas digital direct channels are expanding at a 14.84% CAGR through 2030 of the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

- By geography, the United Kingdom contributed 26.6% of assets of the Europe ETF ŔÖÓăĚĺÓýąŮÍř in 2024; the Nordics region is poised for a 12.65% CAGR to 2030.

Europe ETF ŔÖÓăĚĺÓýąŮÍř Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from mutual funds to low-cost passive vehicles amid MiFID II fee transparency | +2.4% | EU-wide, strongest in UK, Germany, France | Medium term (2�4 years) |

| Proliferation of ESG regulations, such as SFDR Level 2, boosting flows into sustainable ETFs | +1.8% | Concentrated in Nordics, France, Germany | Medium term (2�4 years) |

| Increased adoption of ETFs in pension schemes post the PEPP framework | +1.5% | Early uptake in Netherlands, Denmark, Ireland | Long term (� 4 years) |

| Growth of digital brokerage platforms enabling commission-free ETF savings plans | +1.2% | Germany, UK, France, expanding into Southern Europe | Short term (� 2 years) |

| Expansion of fixed-income ETFs after ECB policy changes | +0.9% | Eurozone, with focus on Germany, France, Italy | Medium term (2�4 years) |

| Cross-border tax harmonization via EU withholding-tax relief pilot, enhancing liquidity | +0.7% | EU-wide, initial benefits in Luxembourg, Ireland, Germany | Long term (� 4 years) |

Source: Mordor Intelligence

Shift from Mutual Funds to Low-Cost Passive Vehicles amid MiFID II Fee Transparency

MiFID II’s granular disclosure rules have forced wealth managers to justify every basis point charged, prompting a pronounced asset shift into ETFs. Advisory firms are redesigning model portfolios around low-cost core allocations, thereby normalizing ETFs as primary building blocks across discretionary mandates. The new pricing clarity also triggered a decline in research coverage for small- and mid-cap issuers, which in turn amplified demand for broadly diversified equity ETFs that require no single-stock analysis. In 2024, European ETF net inflows set a record, confirming that fee transparency is permanently changing investor behavior. These dynamics collectively anchor a durable preference for passive wrappers within the Europe ETF ŔÖÓăĚĺÓýąŮÍř[1]European Central Bank, “Financial Stability Review May 2025,â€� ecb.europa.eu.

Proliferation of ESG Regulations, such as SFDR Level 2, Boosting Flows into Sustainable ETFs

SFDR Level 2 has created a rule-based taxonomy that channels capital toward well-defined sustainability objectives. Managers now segment Article 8 and Article 9 line-ups with clear impact metrics, allowing investors to express environmental or social priorities inside cost-efficient vehicles. Anticipated SFDR 2.0 revisions introduce additional product classes—Sustainable, Transition, ESG Collection, and Unclassified—further sharpening disclosures and accentuating Europe’s first-mover advantage in responsible investing[2]ESMA, “ESG-Related Name Changes and Fund Flows,â€� esma.europa.eu. As allocators recalibrate toward net-zero alignment, sustainable ETFs enjoy stronger organic growth and often command slightly higher fees, counterbalancing industry-wide margin compression. Consequently, ESG regulation is a structural growth catalyst for the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Increased Adoption of ETFs in Pension Schemes Post PEPP Framework

The Pan-European Personal Pension Product establishes a portable, standardized account capped at 1% in total costs, making ETFs the natural fit for meeting that ceiling while ensuring diversified exposure. Early adopters in the Netherlands, Denmark, and Ireland have already incorporated multi-asset ETF allocations into default offerings, signaling that previously fragmented pension silos are converging around unified, low-cost options. An aging demographic across the EU, coupled with persistent funding gaps, intensifies pressure on plan sponsors to maximize risk-adjusted returns at minimal expense. Expected regulatory refinements in 2025, including potential employer contributions, should further scale ETF uptake. Over time, pensions will represent an outsized share of incremental flows into the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Growth of Digital Brokerage Platforms Enabling Commission-Free ETF Savings Plans

Zero-commission trading and fractional share features are redefining retail engagement, particularly among investors aged 18-34. Germany alone hosts more than 9 million ETF savings plans, a figure that could double by 2026 as pan-European platforms replicate its template[3]State Street Global Advisors, “SPDR MSCI Resilient Future UCITS ETF Launch,â€� ssga.com. Daily order-flow patterns show increased retail activity in early-day auctions, providing liquidity provisioning opportunities for authorized participants. As mobile apps remove frictions in account opening, A/B testing of thematic campaigns drives retail discovery of newer ETF niches, from defense to buffer strategies. Digital distribution is therefore expanding penetration into households previously served exclusively by traditional banks, enlarging the addressable base for the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented European exchange landscape elevating trading & settlement costs | -1.3% | EU-wide, most acute in cross-border trades | Medium term (2�4 years) |

| UCITS concentration caps limiting thematic ETF launches | -0.8% | EU-wide, affecting specialized themes | Short term (� 2 years) |

| Regulatory scrutiny on synthetic replication counterparty risk | -0.6% | UK, Luxembourg, Ireland | Medium term (2�4 years) |

| Liquidity concerns during stress episodes (e.g., 2022 LDI crisis) | -0.4% | EU-wide, emphasis on fixed-income ETFs | Short term (� 2 years) |

Source: Mordor Intelligence

Fragmented European Exchange Landscape Elevating Trading & Settlement Costs

Twenty-nine trading venues and heterogeneous clearing houses impede consolidated liquidity and inflate bid-ask spreads. More than half of the 11,000-plus ETF listings trade fewer than 10 times daily, forcing ŔÖÓăĚĺÓýąŮÍř makers to warehouse risk, particularly during volatile sessions. The forthcoming move to T+1 settlement aims to harmonize with United States timing, but creates interim operational complexity given the EU’s current T+2 norm. Industry responses include Euronext’s plan to centralize settlement across Amsterdam, Brussels, and Paris, yet full benefits hinge on multilateral adoption. Until harmonization materializes, structural fragmentation remains a drag on the velocity of flows within the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

UCITS Concentration Caps Limiting Thematic ETF Launches

UCITS rules cap issuer, sector, and index concentrations, constraining exposures that single-theme products often require. Sponsors must engineer synthetic or optimized sampling to stay within limits, prolonging product-development timelines and increasing operational costs. Restrictions can also dilute the purity of certain strategies, thereby reducing investor appeal. While exemptions exist through diversification derivatives, regulatory approval is time-consuming and resource-intensive. The net effect is a slower cadence of launches in niche segments, tempering the speed at which the Europe ETF ŔÖÓăĚĺÓýąŮÍř can meet fast-evolving thematic demand.

Segment Analysis

By Asset Class: Equity Dominates while Alternatives Accelerate

Equity ETFs accounted for a 67.8% share of the Europe ETF ŔÖÓăĚĺÓýąŮÍř in 2024, confirming their status as the core allocation vehicle across portfolios. Bond demand is picking up as the ECB pivots toward looser monetary conditions, and defensive investor sentiment is channeling fresh flows into short-duration government and investment-grade corporate ETFs. Commodities remain primarily tactical instruments, yet gold-linked funds saw solid inflows during early 2025 risk-off episodes, underscoring their role as volatility buffers. Real estate and currency exposures persist as minority allocations, chiefly for hedging or yield-enhancement use cases. Structural tailwinds—fee compression, transparency, and secondary-ŔÖÓăĚĺÓýąŮÍř liquidity—keep equity in pole position even as other asset classes gain relevance.

Alternatives post the fastest trajectory, expanding at a 13.72% CAGR through 2030 as defined-outcome, derivative-income, and buffer products scale. The WisdomTree Europe Defense ETF launch shows how geopolitical funding shifts translate into new exposures, while option-based strategies offer downside mitigation that resonates with cautious retail savers. Fixed-income wrappers have also transformed price discovery in historically opaque bond ŔÖÓăĚĺÓýąŮÍřs, allowing institutional desks to execute portfolio-level adjustments intraday. Blended multi-asset ETFs are emerging, packaging equity, bond, and commodity sleeves under a single umbrella, further broadening appeal. These advances underscore how innovation continues to diversify the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Note: Segment shares of all individual segments available upon report purchase

By Investment Strategy: Active Strategies Challenge Passive Dominance

Passive products captured 90.7% of the Europe ETF ŔÖÓăĚĺÓýąŮÍř in 2024, yet active ETFs are projected to expand at a 15.21% CAGR, signaling the early phase of a structural rebalance. Luxembourg’s removal of subscription tax for active listings and Ireland’s authorization of semi-transparent structures reduce two longstanding operational barriers. Asset managers view active wrappers as convenient channels to distribute proven mutual-fund IP in a lower-cost, exchange-traded format. Fee differentials remain meaningful—active products generally price 15-20 bps higher—yet investors accept the premium when strategies exhibit alpha consistency. As more managers replicate core mutual fund franchises in ETF form, incremental inflows will carve a larger slice of the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Passive leadership nevertheless persists, supported by scale economies in manufacturing and seeding, plus tight expense ratios that can fall below eight basis points on flagship index trackers. Record inflows into core benchmarks during the 2024-2025 period attest to cost sensitivity across both retail and institutional segments. Smart-beta methodologies occupy a middle ground, blending systematic tilts with transparent rule sets, and continue to draw interest from asset allocators seeking factor exposure without full active-manager risk. Traditional ŔÖÓăĚĺÓýąŮÍř-capitalization products therefore remain the foundational building blocks inside model portfolios across the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

By Investor Type: Retail Growth Challenges Institutional Dominance

Institutional investors controlled 62.5% of the Europe ETF ŔÖÓăĚĺÓýąŮÍř in 2024, leveraging ETFs for transition management, liquidity sleeves, and collateral efficiency. Insurance companies, in particular, favor ETFs over swaps or futures to replicate index exposure under Solvency II capital rules. Pension funds adopt multi-asset ETF cores that deliver diversification inside strict fee ceilings, making them early beneficiaries of PEPP roll-outs. Hedge funds utilize liquid fixed-income ETFs to hedge macro risk efficiently during intraday windows. Such use cases keep the institutional bloc central to the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Retail participation is accelerating at an 11.43% CAGR, propelled by commission-free trading apps that lower entry thresholds. UK ownership doubled among investors aged 18-34 between 2022 and 2025, while Germany’s savings-plan culture is exporting to Southern Europe via pan-regional digital brokers. Educational features embedded in mobile interfaces demystify rebalancing and tax-loss harvesting, further driving adoption. Cross-border passporting ensures investors can buy identical tickers irrespective of domicile, enhancing network effects. Over the forecast horizon, retail inflows will form a larger slice of the Europe ETF industry’s expansion story.

By Distribution Channel: Digital Platforms Disrupt Traditional Models

Institutional platforms still processed 37.9% of 2024 flows, with custodians and global brokers facilitating large-block creations and redemptions for asset-management mandates. Banks remain influential in continental ŔÖÓăĚĺÓýąŮÍřs where branch networks distribute in-house advice and packaged portfolios, often blending ETFs and mutual funds to comply with MiFID II suitability tests. Wealth managers increasingly outsource asset allocation to model portfolios centered on low-cost ETFs, freeing time for holistic financial-planning services. These channels collectively reinforce established scale advantages for incumbent sponsors.

Direct-to-consumer platforms are the fastest risers, expanding at a 14.84% CAGR as mobile onboarding compresses account-opening times to minutes. The number of active ETF savings plans surpassed 10 million across Europe in 2024, and algorithmic robo-adviser rebalancing guarantees steady two-way order flow on the exchange. Social-media campaigns, in-app tutorials, and pay-per-trade pricing incentives further widen appeal to younger demographics. With independent advice scarce and costly, self-directed platforms close the guidance gap via bundled research and automated diversification. Digital distribution is therefore pivotal in democratizing the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Geography Analysis

The United Kingdom leads with a 26.6% asset share in 2024, leveraging deep capital ŔÖÓăĚĺÓýąŮÍřs infrastructure and a sophisticated advisory ecosystem that integrates ETFs across discretionary and model portfolio services. Regulatory initiatives such as the Financial Conduct Authority’s liquidity-management guidelines further strengthen ŔÖÓăĚĺÓýąŮÍř resilience, while the planned T+1 transition by 2027 aims to synchronize settlement with US practice and reduce counterparty-risk cycles. Although only 8% of UK retail investors hold ETFs today, rising adoption among millennials signals substantial upside for the Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Germany exemplifies retail momentum, as ETF savings plans have significantly increased in 2024 and are projected to attract substantial annual contributions by 2028. Fiscal stimuli, including the EUR 500 billion infrastructure fund and expanded defense budgets, boost fixed-income issuance and create new thematic opportunities for sector-focused products. The Nordics exhibit the fastest forecast CAGR at 12.65%, supported by widespread digital adoption and policy environments aligned with sustainability objectives. France remains an important node, underpinned by a mature institutional base and growing ESG allocations, while Benelux jurisdictions—particularly Luxembourg—capitalize on domicile advantages and tax incentives for active ETFs.

Eastern European ŔÖÓăĚĺÓýąŮÍřs lag in penetration but present catch-up potential as pan-regional platforms bypass domestic distribution bottlenecks. The European Commission’s Savings and Investment Union initiative seeks to mobilize EUR 11.4 trillion in low-yield bank deposits toward capital ŔÖÓăĚĺÓýąŮÍřs, a structural catalyst for ETFs. Concurrently, Euronext’s consolidation of settlement across Amsterdam, Brussels, and Paris by 2026 promises liquidity pooling and cost reduction. Viewed collectively, geographic differentials are narrowing as digital distribution and regulatory harmonization knit together a more integrated Europe ETF ŔÖÓăĚĺÓýąŮÍř.

Competitive Landscape

The Europe ETF ŔÖÓăĚĺÓýąŮÍř exhibits moderate concentration, with large global managers retaining scale advantages even as niche entrants carve specialized footholds. Established providers leverage decades-old index-manufacturing partnerships, deep seed capital, and extensive ŔÖÓăĚĺÓýąŮÍř-making agreements to deliver tight spreads across flagship products. Nonetheless, fee deflation continues to compress margins, prompting strategic differentiation through thematic innovation, ESG overlays, and share-class architecture that suits varied investor tax profiles.

White-label platforms have lowered the barrier for boutique firms to launch products without erecting full operational stacks, intensifying competitive churn. Several asset owners now operate dual models—distributing proprietary ETFs while also sub-advising mandates for third parties—to capture incremental basis-point earnings. Regulatory reforms support diversity: Ireland’s allowance for ETF share classes within mutual-fund umbrellas and Luxembourg’s subscription-tax exemption for active ETFs make these domiciles attractive for next-generation launches.

Innovation extends beyond product design into technology. Blockchain-enabled share issuance, real-time NAV dissemination, and API-based order routing are under pilot across multiple sponsors. At the same time, ŔÖÓăĚĺÓýąŮÍř-structure initiatives such as standardized settlement and harmonized corporate-action processing seek to level the playing field, thereby reducing scale economies historically enjoyed by the largest issuers. Competitive intensity is therefore rising, yet incumbents remain well-positioned due to broad line-ups, brand recognition, and entrenched relationships with institutional gatekeepers across the European ETF ŔÖÓăĚĺÓýąŮÍř.

Europe ETF Industry Leaders

-

BlackRock � iShares

-

Amundi (incl. Lyxor)

-

DWS � Xtrackers

-

UBS Asset Management

-

Vanguard

- *Disclaimer: Major Players sorted in no particular order

Need More Details on ŔÖÓăĚĺÓýąŮÍř Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Franklin Templeton introduced the US Mega Cap 100 UCITS ETF on Deutsche Börse Xetra and London Stock Exchange with a 0.09% TER.

- April 2025: State Street Global Advisors launched the SPDR MSCI Resilient Future UCITS ETF under SFDR Article 8, embedding a minimum 30% sustainable-investment allocation.

- April 2025: Euronext confirmed the consolidation of settlement for equities and ETFs in Amsterdam, Brussels, and Paris through Euronext Securities by September 2026.

- March 2025: BlackRock removed sustainability terms from 56 funds ahead of anticipated ESMA naming rules, indicating adaptive product positioning.

Europe ETF ŔÖÓăĚĺÓýąŮÍř Report Scope

Europe ETF is an Exchange Traded Fund (ETF) that invests in the Euro, either directly or through euro-denominated short-term debt. Euro ETFs are often established as currency or grantor trusts. Stakeholders include a claim to a specific amount of euros per share. The report covers an understanding and in-depth analysis of the ŔÖÓăĚĺÓýąŮÍř size and forecasts for the various segments of the Europe ETF industry. It includes the regulatory environment, ETF providers, and their business models, along with detailed ŔÖÓăĚĺÓýąŮÍř segmentation, product types, revenues, dividends, current ŔÖÓăĚĺÓýąŮÍř trends, changes in ŔÖÓăĚĺÓýąŮÍř dynamics, and growth opportunities.

The Europe ETF ŔÖÓăĚĺÓýąŮÍř is segmented by ETF types (equity ETF, fixed income ETF, commodity ETF, alternative ETF, money ŔÖÓăĚĺÓýąŮÍř ETF, mixed assets ETF, and others) and country (UK, Germany, France, Italy, Netherlands, Spain, and rest of Europe). The report offers ŔÖÓăĚĺÓýąŮÍř size and forecasts for Europe ETF ŔÖÓăĚĺÓýąŮÍř in value (USD) for all the above segments.

| By Asset Class | Equity ETFs |

| Fixed-Income ETFs | |

| Commodity ETFs | |

| Currency ETFs | |

| Real-Estate ETFs | |

| Alternative ETFs | |

| By Investment Strategy | Active |

| Passive | |

| By Investor Type | Retail |

| Institutional | |

| By Distribution Channel | Direct and Digital Retail Platforms |

| Financial Advisors and Wealth Managers | |

| Institutional Channels | |

| Traditional Banks and Full-Service Brokers | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe |

By Asset Class

| Equity ETFs |

| Fixed-Income ETFs |

| Commodity ETFs |

| Currency ETFs |

| Real-Estate ETFs |

| Alternative ETFs |

By Investment Strategy

| Active |

| Passive |

By Investor Type

| Retail |

| Institutional |

By Distribution Channel

| Direct and Digital Retail Platforms |

| Financial Advisors and Wealth Managers |

| Institutional Channels |

| Traditional Banks and Full-Service Brokers |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Benelux (Belgium, Netherlands, and Luxembourg) |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected growth rate for the Europe ETF ŔÖÓăĚĺÓýąŮÍř between 2025 and 2030?

The Europe ETF ŔÖÓăĚĺÓýąŮÍř is expected to expand at a 10.20% CAGR, rising from USD 2.58 trillion in 2025 to USD 4.20 trillion by 2030.

Which asset class currently dominates European ETF assets?

Equity ETFs lead the way, accounting for 67.8% of assets in 2024, although alternatives are the fastest-growing category.

How quickly are active ETF strategies growing in Europe?

Active ETFs are forecast to grow at a 15.21% CAGR through 2030, compared with passive products that continue to hold the majority of assets.

What role do digital platforms play in European ETF distribution?

Direct-to-consumer digital platforms are the fastest-growing channel, expanding at 14.84% CAGR and enabling a significant number of savings plans across the region.

Which geographic region is expected to grow fastest within the Europe ETF ŔÖÓăĚĺÓýąŮÍř?

The Nordics are set to post a 12.65% CAGR through 2030, driven by advanced digital adoption and strong demand for ESG-aligned products.

What structural change is being implemented to reduce settlement risk in European ETF trading?

Europe plans to transition to T+1 settlement by 2027, aiming to align with US ŔÖÓăĚĺÓýąŮÍřs and enhance post-trade efficiency.